Sitting down with Rick Pudner almost a year after Arabian Business broke the news he was resigning as group CEO of Emirates NBD, there are two things you instantly notice about his appearance. His snow white locks could well be a by-product of leading Dubai’s largest bank through the region’s biggest financial crisis, the fallout from the Dubai World debt restructuring and the late nights in meetings trying to stitch the country’s banking system back together. At the same time, his deep amber tan indicates that he’s been able to get out from behind the desk a bit more. Freedom from the financial headaches of leading a massive banking institution has lent him some time to enjoy the famous Dubai sunshine. And who can blame him? After 24 years at HSBC, he joined Emirates Bank in 2006 as CEO and successfully steered the lender through its merger with local rival National Bank of Dubai (NBD). Then 2008 came along and we all know what happened then. “It was a real crisis point,” he recalls. “At the IMF meeting in 2008 the opinion was that the world was on the verge of Armageddon financially.”

Having helped pull the country back from the edge and worked through those darker days towards the end of the last decade, Pudner can take pride in the fact that Emirates NBD doubled its most recent quarterly net profit, generating $424.7m in the three months to 30 September, something no doubt down to the legacy he left in place. “Progress has been very positive. Look at Dubai now, the growth model seems to be working well and is sustainable. It was a perfect storm [in 2008]. Banks are very well aware of the scope of the risk and a lot more conservative in their approach now. It all looks very positive. The structure now is a lot better,” he says confidently.

So what now? That’s a good question, he concedes. The answer, however, is pretty simple: his focus now is on SMEs, the small and medium-sized companies that are the backbone of Dubai, the UAE and pretty much every country around the world. “I have various non-executive director roles… if you want an exciting place to be it is in the UAE. This is as good as it gets. It is being here and keeping up to date and looking at opportunities as they come along… At the moment, Beehive is the major focus for me.”

The Beehive in question is a new Dubai-based company which is the region’s first peer-to-peer (P2P) online lending platform, offering a new funding alternative for SMEs. While the concept is already established in the US and Europe, it basically brings together investors who want to broaden their investment portfolio and small companies that need capital quickly to drive growth.

“I’m very excited to be part of Beehive and as an alternative finance platform I think it will bring significant benefits to SMEs, investors and the region itself. Presently, a major stumbling block for businesses with growth aspirations is gaining access to credit, as banks generally reject between 50-70 percent of SME loan applications. “SMEs represent 90 percent of total businesses in the UAE but account for just 4 percent of bank loans. Through Beehive, we have created an innovative online platform that directly connects investors and creditworthy businesses creating mutually beneficial partnerships for growth,” Pudner says.

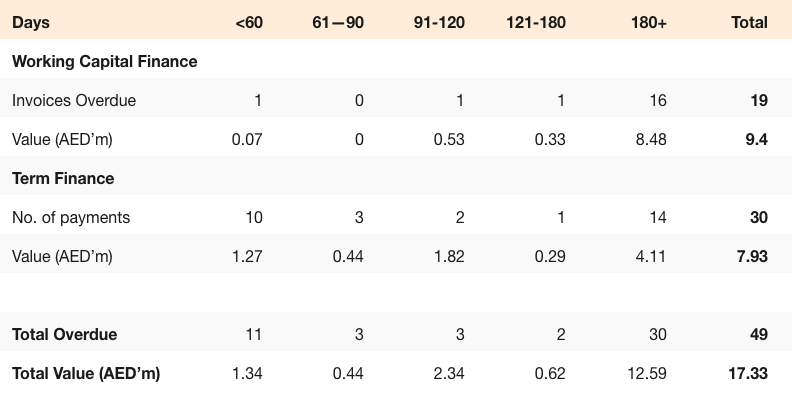

Launched around two months ago, the company has lent in the region of AED2m ($544,507) to six companies, from around 500 investors signed up. The online portal allows established businesses, which have been operating for around two years, seek investment of between AED100,000 and AED500,000, while individual investors can invest from as little as AED100. Similar to eBay or the popular Dragon’s Den TV format, investors can bid to lend money, choosing how much they will lend and the interest rate. The companies seeking investment can then accept or reject the offers. Beehive then facilitates the loan agreement between the business and investors, charging a small percentage fee of the loan amount.

The SMEs generally receive funding in around seven days and investors receive monthly repayments at target rates of between eight and 12 percent. “At its very basic level it is crowdfunding… but if you evolve that,” says Craig Moore, CEO of Beehive. “At its core, you are democratising lending. This has only been possible recently due to technology. You can come onto Beehive and you can open an account for as little as AED1,000 and then you can invest from as little as AED100 to individual businesses.“If you have a business that comes onto the platform and is looking for AED100,000 that may be made up of 100 people at AED1,000 each, which also allows you as an investor to diverse your money into many different businesses and therefore lower your risk.”

So what attracted Pudner to come back into the financial arena and sign up as chairman of Beehive? “Craig approached me at the end of last year and I was in wind-down mode after leaving Emirates NBD and I looked at the proposal. I know a little bit about the funding concepts from the UK and from the US lending club. “I looked at it and I thought it would be an interesting concept and it’s a proven concept in the UK. The timing for me felt right to go down this route of innovation and new technology and helping to fill that gap in the market or access to finance for SMEs. “The key selling proposition for this model is the quick turnaround for SMEs to approach the platform. We access the credit but we can do that within a week, put the SME on the platform and he or she can fulfil their loan requirement within two weeks. It is the speed and the efficiency of the model that drives the price down to get to the optimum level.”

One misconception both men are keen to rule out is, the companies that come to the platform are doing so because they have been rejected by every bank or are in desperate need of capital. “So our stated aim is to be lender of first resort not last resort,” says Moore. “Because if you look at the businesses that have approached us… We predict they can reduce the cost of their finance by 25-30 percent. Plus get access to finance quicker, so it is in an SME’s interest to come to us. “They are not high risk… not at all. We have some stringent criteria and are only looking at businesses that have been profitably trading for two years, have all the necessary documentation and have a good back history and credit track history. We are looking for the strongest possible businesses.”

Determining creditworthiness is an obstacle for banks in the region, Pudner admits, but the advent of certain tools and even the newly launched Al Etihad Credit Bureau is showing signs that things are getting better. Companies launched on the Beehive platform are also rigorously checked to make sure they are not credit risky. “We have our own credit model and our credit teams have worked in this region in the UAE space for the last seven or eight years. We use credit reference tools so we can take a holistic approach, which is what the banks use too.”

Blank cheques are also a common element of the lending infrastructure in the UAE, in order to give the lender some security, and Moore admits that this is something that has been adopted by Beehive. “It is part of the wider protection for investors. Just as they would do if taking a bank loan,” says Moore. “Obviously we are working with the current system. We are working within the system,” adds Pudner.

However, when the thorny issue of whether this system should be amended and bouncing a cheque should be decriminalised is raised, he resorts to the media training he learnt while at the bank. “There has been a lot of talk about looking at that and direct debits coming in. I haven’t got a personal view. It is a system that has been used for whatever period of time and at the moment it works. It does put a burden on the infrastructure here if you have to make a criminal case over AED500. In terms of police time, there are probably more effective ways of doing it,” he says without giving too much away.

In order for the SMEs to obtain their capital, Beehive also needs to attract investors eager to inject money into the small companies. But I do wonder what is to stop Beehive being hijacked by those looking to launder some shady funds?

“For everyone we do KYC [Know Your Customer] and AML [Anti-Money Laundering] checks and our third-party partner, who is a global fund administrator, has to sign off on every investor. [They do] all the usual checks that any financial institution does to make sure they are of the right nationality and tick all the boxes,” assures Moore.

Beehive certainly has ambitious plans to grow big, quickly. “We have started in the UAE and we see the UAE as a base to go into other territories,” says Moore. “We are looking into those, some close, some further afield. We are a private business and privately funded. We will continue to raise finance. We have about 15 staff so we will turn a profit in year three, so the classic technology curve.”

It is certainly a format that has caught Pudner’s eye and one be believes strongly in. “There is a well-documented funding gap in the Middle East. There is always going to be a gap. This model helps to fill that gap.

“If you look back at the UK, in the doldrums days, the government was incessantly saying banks have to lend more to SMEs. There weren’t any direct quotas but the reality was it didn’t really get done and that is why the government is now putting money into platforms,” he says.

“As you get more investors, you get more business interest and it encourages more investors. This year I think there is going to be $9bn lent by platforms as an industry. This is forecast to grow to $1 trillion by 2025, so what you are seeing is a wave of movement and there will be more and more.”

Having gone from billion-dollar deals to small and medium sized investors, this certainly seems to be a wave Pudner is happy to keep surfing for the time being.

Source: Arabian Business