Since launching his fintech startup Beehive four years ago, Craig Moore has given small businesses in Dubai a new way to raise capital through peer-to-peer lending.

A little over a year ago, Stevi Lowmass needed funds to grow her small Dubai soap-making business. Previously, she borrowed about $68,000 from Rakbank at 25% interest—typical for small businesses in Dubai. Lowmass was also saddled with a number of unexpected charges and felt the loan officer hand’t been transparent with her. “Our accountant and I had to take the loan schedule and work out the interest rate ourselves,” says Lowmass.

So when she needed to raise more funds, she decided to look elsewhere. She found Beehive, a Dubai-based peer-to-peer lending platform. Through Beehive, Lowmass borrowed $54,000 in late 2016 at an interest rate of 9.89%. Although it took about the same amount of time to get a loan from Beehive as it did through the bank, Lowmass says, “the funds were raised cleanly and extremely quickly and we were delighted with the resulting interest rate we ended up paying.”

Lowmass is one of a growing number of small business owners in the U.A.E. who’ve raised capital through peer-to-peer lending in recent years. It allows small businesses that don’t have recourse to venture capital or bank loans, to borrow directly from a crowd of retail investors at lower rates.

Regionally, four-year-old Beehive is an early mover. Another is liwwa, formed in 2013 in Jordan. Beehive founder Craig Moore, a 45-year-old British expat in Dubai, says his platform has served as an intermediary, so far, for 250 funding requests thanks to an explosion of startups. It has 6,000 registered investors—mostly from the U.A.E.—and has channeled a total of $40 million to borrowers.

Globally, peer-to-peer lending gained ground in the aftermath of the 2008 financial crisis, when banks cut back on loans. Led by U.K.’s Funding Circle and U.S.-based Lending Club, this alternative form of finance could command $1 trillion globally by 2025, up from an estimated $64 billion in 2015, according to U.S.-based statistics firm Statista.

Until a year ago Beehive operated largely on the margins of the U.A.E.’s financial sector. It got a formal license in March 2017 when the Dubai Financial Services Authority (DFSA) issued rules around peer-to-peer lending. New regulations in Dubai and Bahrain signaled they were embracing fintech, leading to the introduction of fintech funds and accelerators.

Regulatory blessing helped Beehive secure $5 million in a first venture round led by Riyad Taqnia Fund in December 2017. At the urging of investors, Moore is exploring entering the Saudi market this year and expects to launch in Thailand by spring.

According to Ivo Detelinov, who heads private equity funds at Riyad Capital- one of the partners behind the Riyad Taqnia Fund- companies like Beehive could play a significant role in the Kingdom as the country looks to accelerate SME growth. “We believe Beehive fits very nicely in this evolving SME ecosystem,” says Detelinov.

Beehive’s growth has been underpinned by a tough lending environment for SMEs in the region. While Dubai has encouraged the creation of small businesses, access to finance remains difficult. According to the Khalifa Fund for Enterprise Development, a fund launched by Abu Dhabi’s government to facilitate entrepreneurship development and SME growth, loans to SMEs account for 4% of outstanding bank credit in the U.A.E., below the regional average of 9.3%. “There are a lot of banks here, but those banks aren’t lending [to SMEs],” says Moore.

Reason: some banks don’t want to bother with smaller loans, or are reluctant to lend to high-risk ventures. When they do, interest rates can be in the prohibitive range of 18% to 20%.

Still, peer-to-peer lending isn’t a cinch for prospective borrowers. Beehive received an average of 20 requests for funding a week in 2017, and rejected more than 80%—a high bar considering that banks reject 50% to 70% of SME funding applications, according to the Khalifa Fund.

To borrow through Beehive, companies must be U.A.E.-based, at least two years old and have annual revenue in excess of $680,000, among other requirements. The startup built its own risk models to determine the creditworthiness of borrowers. Beehive can approve funding requests in less than three days, and lends between $27,000 and $272,000 on terms ranging from six months to three years.

Investors bid on different loan amounts—as little as $27—at varying interest rates, with the lowest rate winning. Moore says investors average returns of 12% per year. They tend to be bankers, lawyers and accountants who generally invest between $2,500 and $8,000. Beehive charges them a 2% annual fee from the repayments they collect, while businesses pay between 2% and 4% of the principal amount borrowed when the loan is completed.

Beehive also processes Sharia-compliant finance requests, having received a certification from the Sharia advisory company Shariyah Review Bureau.

As it’s forbidden under Sharia to earn money from lending cash alone, Beehive uses the Islamic financing structure known as Murabaha to process these funding requests. Under this arrangement, the loan is structured as an asset-backed transaction, where the lender buys a commodity on behalf of the borrower and resells it to them at an agreed-upon markup, paid back in installments.

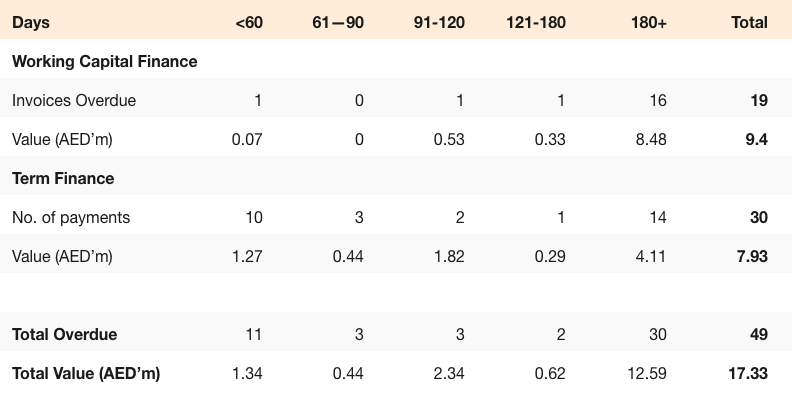

Of course, there’s risk. Loans are unsecured, and Beehive’s rate of nonperforming loans is 1.2%. “Inevitably, you will get defaults in this,” says Moore. By comparison, more than 20% of exposures to SMEs were classified as non-performing in 2016, according to a report from the Central Bank of the U.A.E. last year.

Last summer, Beehive signed an agreement to facilitate SME financing with the Mohammed Bin Rashid Fund (MBRF), which is the financial arm of the governmental organization Dubai SME. Under the agreement, the fund will provide a capital guarantee that investors will be paid back if certain borrowers default. In order to qualify for the MBRF capital guarantee, a business must be both Emirati-owned and Sharia compliant.

Although Beehive’s base of retail investors continues to grow, Moore worries he might not have enough money to lend. “We can only help finance when there’s liquidity,” he says. He’s trying to attract institutional investors. “We’re talking to banks about how we could collaborate and distribute some of their balance sheet,” he says.

That’s quick progress from just five years ago. “Nobody was talking about fintech in 2013,” says Moore.

Born and raised near Manchester, U.K., Moore worked in various sales, consulting and finance roles at companies including Dell, HSBC, and Hitachi. In 2009, he founded a data analysis company and sold it to IBM three years later. He became interested in peer-to-peer lending after trying it out. He invested through a couple different platforms in the U.K., securing returns of between 6-7%.

It was already a crowded landscape in the U.K., so he looked at opportunities elsewhere. He knew Dubai and had friends there. “It was a market that had an opportunity for us immediately,” he says, even if fintech wasn’t then a buzzword. He moved in 2014, bringing with him his former head of technology.

Through an acquaintance, Moore met Rick Pudner, the former Group CEO of Emirates NBD, who expressed an interest in peer-to-peer lending. He joined as chairman of Beehive.

It was a coup for the fledgling startup. “We were launching a new concept in a new market. Bringing Rick on showed this was a strong management team trying to do things the right way,” says Moore.

Funding Beehive was another issue. Because regulations around peer to- peer lending were fuzzy, Moore couldn’t interest VCs. Instead, he ended up raising $2.5 million from 42 individuals—all people that either he or his management team knew, which they used to fund development. To add credibility, he modeled the company’s operations on the U.K.’s Financial Conduct Authority’s best practices for peer-to-peer lenders. In early 2014, the FCA introduced guidance for crowdfunding and peer-to-peer lending, one of the first prominent regulators to do so.

“I think a lot of people were of the view this would never work here,” says Moore. But as fintech gains more prominence in the region, things are looking brighter.

– By: Samuel Wendel, Forbes Middle East