P2P (peer-to-peer) lending is an exciting and different way to invest your money. It can be a great option for people who want to earn higher returns on their investments but don’t want to go through the hassle of managing individual stocks or bonds. However, like all types of investments, there are associated risks that are important to understand. With this in mind, we’ve compiled a comprehensive overview of the potential risks and how Beehive works hard to reduce them.

Risk of loans being unsecured

All Beehive loans are unsecured, meaning that they are not backed by any form of tangible asset. Instead, P2P lenders, such as Beehive, take SMEs through a rigorous credit assessment to ensure they are creditworthy and able to repay their loans using a Credit Decisioning Engine. More on this later in the blog.

Despite not having any physical security, this does not mean that Beehive has no recourse in the event of a default or non-performing loan. For every credit facility, Beehive will obtain a Personal Guarantee along with a security cheque for the full value of the facility. This enables Beehive to have both civil and criminal recourse in the event of non-payment and gives Beehive the best chance of collecting investor funds.

Flight risk of the borrower

Beehive refers to flight risk as the risk associated to a borrower receiving funds and fleeing the UAE back to their home country. To mitigate this risk, Beehive performs a series of credit checks against not only the borrowing SME but all the underlying shareholders. Shareholder checks are centered around two main things: how committed the shareholders are to the SME; and how committed the shareholders are to the UAE. Within each of these two sections, Beehive has various credit metrics that assess the associated risk, after which the flight risk can be objectively scored.

Credit risk of the borrowing SME

Beehive has a tried and tested credit scoring algorithm, known as the previously mentioned Credit Decisioning Engine, that has been used and improved since its launch in 2014. The result of this scoring methodology is a default rate of under 2%. In addition to the scoring algorithm, the Beehive Credit team performs a rigorous credit assessment that acts as the foundation of any credit decision. The Beehive Credit team has extensive regional experience and is well-equipped to accurately assess the credibility of any borrowing SME, regardless of the type of credit facility they are requesting.

Risk of recession or market downturn

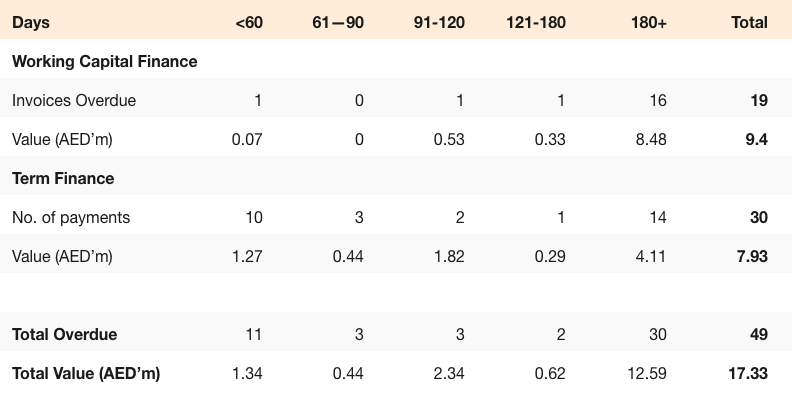

Like any investment into the SME sector, there is always the chance that the ability of the SME to repay could be influenced by the macroeconomic climate of the UAE and associated sectors. This was never more evident than during COVID-19 when many SMEs struggled to not only repay debt but stay in business. During this time the Beehive collections team followed a meticulous collections process that allowed for flexibility around repayment from the borrower, whilst also acting in the best interest of the investors. Beehive takes great pride in the fact that over 80% of non-performing loans during COVID were collected, and it is because of this that Beehive remains confident of replicating this during times of macroeconomic recession.

Fraud risk

Fraud risk is defined as the risk associated to lend to an SME that has submitted a fraudulent loan request. A loan request would be defined as fraudulent if the SME and its management team were to apply for a loan under false pretenses with no material purpose. This risk is mitigated through the points raised in sections 1,2 & 3 of this article but is further mitigated through Beehive’s in-depth compliance check performed on both the SME and its shareholders. Through this compliance check, Beehive can identify various types of suspicious activity, either within the documentation submitted by the SME or through the screening tools used by Beehive Compliance.