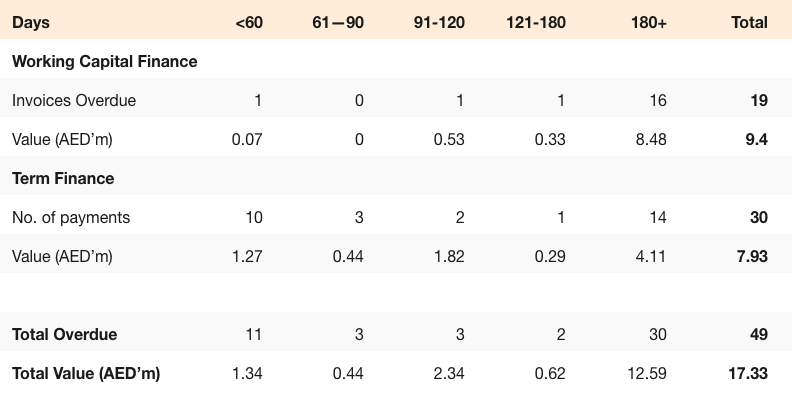

At Beehive we take our duty of care very seriously, and as such we treat investors’ money like it’s our own, protecting it to the best of our ability. Prior to every loan and facility offered, we carry out a thorough credit assessment to ensure it can be repaid.

However, unfortunately there are circumstances that we aren’t able to foresee, which result in either late repayment or default. It is an absolute last resort for Beehive to declare a default, and this article explains what happens from the moment a repayment is one day overdue, until it’s marked as a default, and the efforts we go to to get investors’ money back.

Repayment is overdue

Our system is designed to flag overdue repayments and as soon as we receive a notification we contact the Business to find out why. More often than not, it’s nothing serious so a gentle reminder to make payment normally works.

Agree repayment date

It’s important for us to find out why the SME didn’t make the payment on time and if there’s anything we can do to assist. If the SME isn’t able to make payment within 30 days of the original due date, then Beehive and the SME will agree on a repayment date that can be adhered to. Beehive then recalculates the installment amount (Invoice Finance Only) so investors’ can see the revised payment date and know the additional interest they are due to receive.

Site visit

If either the next installment or the revised repayment date is missed, then a representative from Beehive will visit the business to ensure everything is operational. The representative will enquire with management the reasons for the ongoing delays. If necessary, Beehive will request further documentation to verify these responses. If Beehive are not confident with the reasons given, we may feel it necessary to carry out further investigations such as credit checks, police checks or enquiries from the business’s employees etc.

Non Performing Loan

If the repayments are not brought current within 60 days of the original repayment date then Beehive classifies the loan as a non-performing (NPL). Once a loan is classified as an NPL Beehive will start a full Legal and Civil Case to enforce the repayments.

Legal and Civil cases

Legal Case- Beehive will cash the security cheque and use the returned cheque to initiate a police case. All security cheques are at least AED200k (even if the loan or facility isn’t that amount) meaning that once the cheque has been presented, and subsequently rejected due to insufficient funds, it is classed as a criminal act. Once the police case is opened the police will actively seek the individual/s and they will be arrested. They can then either pay in full to clear the case, stay in prison until the court hearing or bail themselves. If they choose the latter, the police will impose a travel ban still so the individual/s are unable to leave the UAE.

Civil Case- Beehive will also initiate a civil case simultaneously to maximise the chance of recovery and minimise delays.

Default

Beehive will only mark a business as default if the business or its owners are unable to pay within the foreseeable future (not more than a year). A default can be marked from either day one, during / following one of the above mentioned stages, or, if it’s apparent the individual/s have left the UAE, prior to our case being initiated. It differs case by case, and depends whether the cost verses expected recoverable amount is positive. However, once a business is marked as default it does not mean Beehive will stop its recovery efforts. All police cases will be left open and international agents will be utilised (if necessary). Any and all inflows from these future efforts will then be remitted back to the investors upon collection.